Public Accounts 2020-2021 Section I: Consolidated Financial Statements

Jump to:

- Transmittal Letter

- Statement of Responsibility

- Independent Auditors Report

- Consolidated Statements of Financial Position

- Consolidated Statement of Operations and Accumulated Surplus

- Consolidated Statement of Change in Net Debt

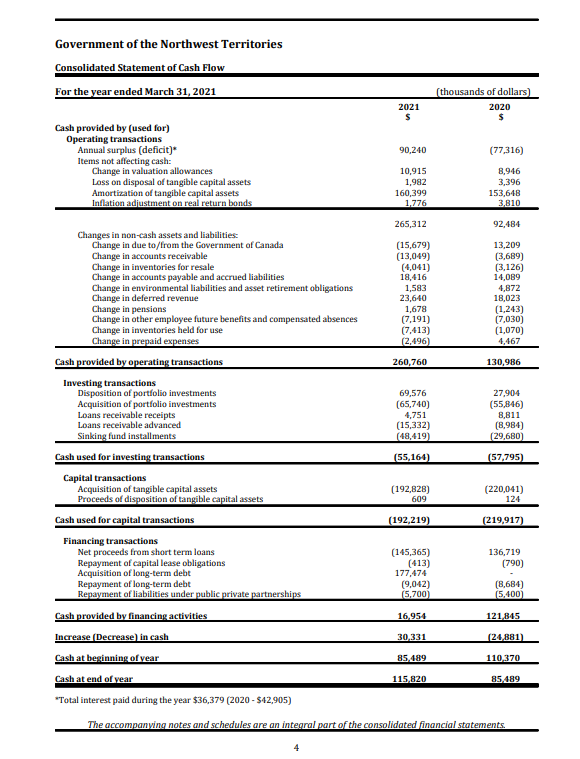

- Consolidated Statement of Cash Flow

- Notes to Consolidated Financial Statements

- Schedule A - Consolidated Schedule of Tangible Capital Assets

- Schedule B - Consolidated Schedule of Segmented Information

- Financial Statement Discussion and Analysis

Transmittal Letter

THE HONOURABLE MARGARET M. THOM

COMMISSIONER OF THE NORTHWEST TERRITORIES

I have the honour to present the Public Accounts of the Northwest Territories in accordance with Sections 37 through 43 of the Northwest Territories Act (Canada), S.C. 2014, c.2, s.2, and Sections 34 through 35 of the Financiai Administration Act, S.N.W.T. 2015, c.l3, for the fiscal year ended March 31, 2021.

Original signed by

Honourable Caroline Wawzonek

Minister of Finance

November 29, 2021

Statement of Responsibility

RESPONSIBILITY FOR FINANCIAL REPORTING

The preparation of the consolidated financial statements of the Government of the Northwest Territories (the Government), and related information contained in the Public Accounts, is the responsibility of the Government through the Office of the Comptroller General.

The consolidated financial statements have been prepared in accordance with Canadian public sector accounting standards (PSAS). Where PSAS permits alternative accounting methods, management has chosen those that are most appropriate. Where required, management's best estimates and judgment have been applied in the preparation of these consolidated financial statements.

The Government fulfills its accounting and reporting responsibilities, through the Office of the Comptroller General, by maintaining systems of financial management and internal control. The systems are continually enhanced and modified to provide timely and accurate information, to safeguard and control the Government's assets, and to ensure that all transactions are in accordance with the Northwest Territories Act and regulations, and the Financial Administration Act of the Northwest Territories and regulations.

The Auditor General of Canada performs an annual audit on the consolidated financial statements in order to express an opinion as to whether the consolidated financial statements present fairly, in all material respects, the financial position of the Government, the results of its operations, the change in its net debt, and its cash flows for the year in accordance with PSAS. During the course of the audit, she also examines transactions that came to her notice, to ensure they are, in all material respects, within the statutory powers of the Government and those organizations included in the consolidated financial statements.

Originally signed by

Julie Mujcin, CPA, CGA

Comptroller General

Government of the Northwest Territories

November 29, 2021

Independent Auditors Report

To the Legislative Assembly of the Northwest Territories

Report on the Audit of the Consolidated Financial Statements

Opinion

We have audited the consolidated financial statements of the Government of the Northwest Territories and its controlled entities (the Group), which comprise the consolidated statement of financial position as at 31 March 2021, and the consolidated statement of operations and accumulated surplus, consolidated statement of change in net debt and consolidated statement of cash flow for the year then ended, and notes to the consolidated financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the consolidated financial position of the Group as at 31 March 2021, and the consolidated results of its operations, consolidated changes in its net debt, and its consolidated cash flows for the year then ended in accordance with Canadian public sector accounting standards.

Basis for Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Consolidated Financial Statements section of our report. We are independent of the Group in accordance with the ethical requirements that are relevant to our audit of the consolidated financial statements in Canada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Other Information

Management is responsible for the other information. The other information comprises the information included in Section I of the Public Accounts 2020–2021, but does not include the consolidated financial statements and our auditor’s report thereon.

Our opinion on the consolidated financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the consolidated financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the consolidated financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and Those Charged with Governance for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with Canadian public sector accounting standards, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, management is responsible for assessing the Group’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless an intention exists to liquidate the Group or to cease operations, or there is no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Group’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Canadian generally accepted auditing standards will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements.

As part of an audit in accordance with Canadian generally accepted auditing standards, we exercise professional judgment and maintain professional skepticism throughout the audit.

We also:

- Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

- Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Group’s internal control.

- Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

- Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Group’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Group to cease to continue as a going concern.

- Evaluate the overall presentation, structure and content of the consolidated financial statements, including the disclosures, and whether the consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

- Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the Group to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision, and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Report on Compliance with Specified Authorities

Opinion

In conjunction with the audit of the consolidated financial statements, we have audited transactions of the Government of the Northwest Territories and its controlled entities coming to our notice for compliance with specified authorities. The specified authorities against which compliance was audited are the Northwest Territories Act and regulations, the Financial Administration Act of the Northwest Territories and regulations, and the specific operating authorities disclosed in Note 1(a) to the consolidated financial statements.

In our opinion, the transactions of the Government of the Northwest Territories and its controlled entities that came to our notice during the audit of the consolidated financial statements have complied, in all material respects, with the specified authorities referred to above.

Responsibilities of Management for Compliance with Specified Authorities

Management is responsible for the Government of the Northwest Territories and its controlled entities’ compliance with the specified authorities named above, and for such internal control as management determines is necessary to enable the Government of the Northwest Territories and its controlled entities to comply with the specified authorities.

Auditor’s Responsibilities for the Audit of Compliance with Specified Authorities

Our audit responsibilities include planning and performing procedures to provide an audit opinion and reporting on whether the transactions coming to our notice during the audit of the consolidated financial statements are in compliance with the specified authorities referred to above.

Originally signed by

Karen Hogan, FCPA, FCA

Auditor General of Canada

Ottawa, Canada

29 November 2021

Consolidated Statements of Financial Position

Consolidated Statement of Operations and Accumulated Surplus

Consolidated Statement of Change in Net Debt

Consolidated Statement of Cash Flow

Notes to Consolidated Financial Statements

(All figures in thousands of dollars)

1. AUTHORITY AND OPERATIONS

(a) Authority and reporting entity

The Government of the Northwest Territories (the Government) operates under the authority of the Northwest Territories Act (Canada). The Government has an elected Legislative Assembly which authorizes all disbursements, advances, loans and investments unless specifically authorized by statute.

The consolidated financial statements have been prepared in accordance with the Northwest Territories Act (Canada) and the Financial Administration Act of the Northwest Territories. The consolidated financial statements present summary information and serve as a means for the Government to show its accountability for the resources, obligations and financial affairs for which it is responsible. The following lists the organizations comprising the Government reporting entity, which are fully consolidated in the financial statements, and their specific operating authority.

Education Act

- Beaufort-Delta Divisional Education Council

- Commission scolaire francophone Territoires du Nord-Ouest

- Dehcho Divisional Education Council

-

Dettah District Education Authority

-

N'dìlo District Education Authority

-

Sahtu Divisional Education Council

-

South Slave Divisional Education Council

-

Yellowknife Public Denominational District Education Authority (Yellowknife Catholic Schools)

-

Yellowknife District No.1 Education Authority

Aurora College Act

-

Aurora College

Hospital Insurance and Health and Social Services Administration Act

-

Hay River Health and Social Services Authority

-

Northwest Territories Health and Social Services Authority

Tlicho Community Services Agency Act

-

Tlicho Community Services Agency

Northwest Territories Business Development and Investment Corporation Act

-

Northwest Territories Business Development and Investment Corporation

Northwest Territories Housing Corporation Act

-

Northwest Territories Housing Corporation

Human Rights Act

-

Northwest Territories Human Rights Commission

Northwest Territories Societies Act

-

Arctic Energy Alliance

Status of Women Council Act

-

Status of Women Council of the Northwest Territories

Northwest Territories Heritage Fund Act

-

Northwest Territories Heritage Fund

Northwest Territories Waters Act

-

Inuvialuit Water Board

Northwest Territories Hydro Corporation Act

-

Northwest Territories Hydro Corporation (NT Hydro)

Northwest Territories Surface Rights Board Act

-

Northwest Territories Surface Rights Board

1. AUTHORITY AND OPERATIONS (continued)

(a) Authority and reporting entity (continued)

All organizations included in the Government reporting entity have a March 31 fiscal year-end with the exception of Aurora College, Divisional Education Councils and District Education Authorities, which have a fiscal year-end of June 30. Transactions of these educational organizations that have occurred during the period to March 31, 2021 and that significantly affect the consolidation have been recorded. Revolving funds are incorporated directly into the Government's accounts while trust assets administered by the Government on behalf of other parties (note 16) are excluded from the Government reporting entity. Revolving Funds are segments of the Government that are engaged in commercial activities, with undefined and non-lapsing expense authority.

(b) Budget

The consolidated budget figures are the appropriations approved by the Legislative Assembly and the approved budgets for the consolidated entities, adjusted to eliminate budgeted inter-entity revenues and expenses. They represent the Government's original consolidated fiscal plan for the year and do not reflect supplementary appropriations.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

These consolidated financial statements are prepared in accordance with Canadian public sector accounting standards as issued by the Public Sector Accounting Board of the Chartered Professional Accountants of Canada.

(a) Measurement uncertainty

The preparation of consolidated financial statements in accordance with Canadian public sector accounting standards requires the Government to make estimates and assumptions that affect the amounts of assets, liabilities, revenues and expenses reported in the consolidated financial statements. By their nature, these estimates are subject to measurement uncertainty. The effect on the consolidated financial statements of changes to such estimates and assumptions in future periods could be significant, although, at the time of preparation of these consolidated statements, the Government believes the estimates and assumptions to be reasonable.

The more significant management estimates relate to environmental liabilities, asset retirement obligations, contingencies, revenue accruals, allowances for doubtful accounts for accounts receivable, valuation allowances for loans receivable, and amortization expense. Other estimates, such as the Canada Health Transfer payments, Canada Social Transfer payments, and Corporate and Personal Income Tax revenues are based on estimates made by the Government of Canada's Department of Finance and are subject to adjustments in future years.

(b) Cash

Cash is comprised of bank account balances, net of outstanding cheques and short-term highly liquid investments that are readily convertible to cash with a maturity date of 90 days or less from the date of acquisition.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(c) Portfolio investments

Portfolio investments are long-term investments in organizations that do not form part of the government reporting entity and are accounted for by the cost or amortized cost method. Such investments are normally in shares and bonds of the investee. When there has been a loss in value of a portfolio investment that is other than a temporary decline, the investment is written down to recognize the loss and it is included as a component of investment income. Interest income is recorded on the accrual basis, dividend income is recognized as it is declared and capital gains and losses are recognized when realized.

(d) Inventories

Inventories for resale consist mainly of bulk fuels, liquor products, and arts and crafts. Bulk fuels are valued at the lower of weighted average cost and net realizable value. Liquor products are valued at the lower of cost and net realizable value. Inventories held for use by NT Hydro consist of materials and supplies, lubricants, critical spare parts, and fuel and are recorded at cost as determined using the weighted average cost method. The remaining inventories held for use (including housing materials and supplies, and hospital supplies) are valued at the lower of cost, determined on a first in, first out basis, and net replacement value. Impairments, when recognized, result in write-downs to net realizable value.

(e) Loans receivable

Loans receivable and advances are stated at the lower of cost and net recoverable value. Valuation allowances, determined on an individual basis, are based on past events, current conditions and all circumstances known at the date of the preparation of the consolidated financial statements and are adjusted annually to reflect the current circumstances by recording write downs or recoveries, as appropriate. Write- downs are recognized when the loans have been deemed uncollectable. Recoveries are recorded when loans previously written down are subsequently collected. Interest revenue is recorded on an accrual basis. Interest revenue is not accrued when the collectability of either principal or interest is not reasonably assured.

(f) Sinking fund

The sinking fund is externally restricted cash held specifically for the purpose of repaying outstanding debt at maturity. The sinking fund is recorded at amortized cost.

(g) Liabilities

Liabilities are present obligations arising from past transactions or events, the settlement of which is expected to result in the future sacrifice of economic benefits.

Accounts payable and accrued liabilities primarily include obligations to pay for goods and services acquired prior to year-end, provide authorized grants and contributions where eligibility criteria are met, and to pay for employee compensation earned prior to year-end.

Bonds and debentures included in long-term debt are recognized at amortized cost (initial cost, less unamortized discount and issuance costs).

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(h) Tangible capital assets and leases

Tangible capital assets are buildings, roads, equipment, etc. whose life extends beyond the fiscal year, original cost exceeds $50 and are intended to be used on an ongoing basis for delivering programs and services. Individual assets less than $50 are expensed when purchased. Tangible capital assets are recorded at cost or where actual cost is not available, estimated current replacement cost, discounted back to the acquisition date. Costs include contracted services, materials and supplies, direct labour, attributable overhead costs, and directly attributable interest. Capitalization of interest ceases when no construction or development is taking place or when a tangible capital asset is ready for use in producing goods or delivering services. Assets, when placed in service, are amortized on a straight-line basis over their estimated useful lives as follows:

The estimate of the useful life of tangible capital assets is reviewed on a regular basis and revised where appropriate on a prospective basis. The remaining unamortized portion of a tangible capital asset may be extended beyond its original estimated useful life when the appropriateness of such a change can be clearly demonstrated.

Write-downs and write-offs of tangible capital assets are recognized whenever significant events and changes in circumstances and use suggest that the asset can no longer contribute to program or service delivery at the level previously anticipated. A write-down is recognized when a reduction in the value of the asset can be objectively measured. A write-off is recognized when the asset is destroyed, stolen, lost, or obsolete to the Government.

Tangible capital assets under construction or development are recorded as work in progress with no amortization until the asset is placed in service. Capital lease agreements are recorded as a liability and a corresponding asset based on the present value of the minimum lease payments, excluding executory costs. The present value is based on the lower of the implicit rate or the Government's borrowing rate at the time the obligation is incurred. Operating leases are charged to expenses. All intangibles, works of art, historical treasures and items inherited by right of the Crown, such as Crown lands, forests, water and mineral resources are not recognized in these consolidated financial statements.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(i) Pensions and other employee future benefits and compensated absences

All eligible employees participate in the Public Service Pension Plan administered by the Government of Canada. The Government's contributions are charged as an expense on a current year basis and represent the total pension obligations. The Government is not required under present legislation to make contributions with respect to any actuarial deficiencies of the Public Service Pension Plan.

Pension benefits to Members of the Legislative Assembly and judges are reported on an actuarial basis. This is done to determine the current value of future entitlement and uses various estimates. When actual experience varies from estimates or when actuarial assumptions change, the adjustments are amortized on a straight-line basis over the estimated average remaining service lives of the contributors. Recognition of actuarial gains and losses commences in the year following the effective date of the related actuarial valuations. In addition, immediate recognition of a previously unrecognized net actuarial gain or loss may be required upon a plan amendment, curtailment or settlement.

Under the terms and conditions of employment, government employees may earn non-pension benefits for resignation, retirement and removal costs. Eligible employees earn benefits based on years of service to a maximum entitlement based on terms of employment. Eligibility is based on a variety of factors including place of hire, date employment commenced, and reason for termination. Benefit entitlements are paid upon resignation, retirement or death of an employee. The expected cost of providing these benefits is recognized as employees render service. Termination benefits are also recorded when employees are identified for lay- off. Compensated absences include sick, special, parental and maternity leave. Accumulating non-vesting sick and special leave are recognized in the period the employee provides service, whereas parental and maternity leave are event driven and are recognized when the leave commences. An actuarial valuation of the cost of these benefits (except maternity and parental leave) has been prepared using data provided by management and assumptions based on management's best estimates.

(j) Contractual obligations and contingent liabilities

The nature of the Government's activities requires entry into contracts that are significant in relation to its current financial position or that will materially affect the level of future expenses. Contractual obligations pertain to funding commitments for operating, commercial and residential leases, and capital projects. Contractual obligations are obligations of a government to others that will become liabilities in the future when the terms of those contracts or agreements are met.

The contingent liabilities of the Government are potential liabilities which may become actual liabilities when one or more future events occur or fail to occur. If the future event is considered likely to occur and is quantifiable, an estimated liability is accrued. If the occurrence of the confirming future event is likely but the amount of the liability cannot be reasonably estimated or if the occurrence of the confirming future event is not determinable, the contingent liability is disclosed.

(k) Contractual rights and contingent assets

The nature of the Government's activities requires entry into contracts that are significant in relation to its current financial position or that will materially affect the level of future revenues. Contractual rights pertain to rights to economic resources arising from contracts or agreements that will result in both an asset and revenue in the future when the terms of contracts or agreements are met.

The contingent assets of the Government are potential assets which may become actual assets when one or more future events occurs or fails to occur. If the future event is considered likely to occur and is quantifiable, an estimated asset is disclosed.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(l) Foreign currency translation

Monetary assets and liabilities denominated in foreign currencies are translated into Canadian dollars using exchange rates at year-end. Foreign currency transactions are translated into Canadian dollars using rates in effect at the time the transactions were entered into. All exchange gains and losses are included in annual surplus (deficit) for the year according to the activities to which they relate.

(m) Projects on behalf of third parties

The Government undertakes projects for the Government of Canada, the Government of Nunavut and others. Where the agreement allows, the Government receives accountable advances and any unexpended balances remaining at year-end are recorded as liabilities in accounts payable and accrued liabilities or due to the Government of Canada, as applicable. Recoveries are accrued when expenses as allowed under the project contract, exceed advances and are recorded as receivables in accounts receivable or due from the Government of Canada, as applicable.

(n) Grant from the Government of Canada

Under Federal-Provincial Fiscal Arrangements Act (Canada), the Grant from the Government of Canada is based on the Territorial Formula Financing calculated as the Gross Expenditure Base, offset by eligible revenues, which are based on a three-year moving average, lagged two years, of representative revenue bases at national average tax rates. Population growth rates and growth in provincial/local government spending are variables used to determine the growth in the Gross Expenditure Base. The Grant is calculated once for each fiscal year and is not revised, with all payments flowing to the Government prior to the end of the fiscal year.

(o) Transfer payments

Government transfers are recognized as revenue in the period in which the events giving rise to the transfer occurred, as long as the transfer is authorized, eligibility criteria have been met, stipulations that give rise to a liability have been satisfied and a reasonable estimate of the amount can be made. Transfers received before these criteria are fully met are recorded as deferred revenue. Transfers received for tangible capital assets are recognized as revenue when the tangible capital asset is put into service.

(p) Taxes, regulatory, resource, and general revenues

Corporate and Personal Income tax revenue are recognized on an accrual basis, net of any tax concessions. Income tax is calculated net of tax deductions and credits allowed under the Income Tax Act (Canada). If an expense provides a financial benefit other than a relief of taxes, it is classified as a transfer made through the tax system. If an expense provides tax relief to a taxpayer and relates to revenue, this expense is considered a tax concession and is netted against tax revenues. Taxes, under the Income Tax Act (Canada), are collected by the Government of Canada on behalf of the Government under a tax collection agreement. The Government of Canada remits Personal Income taxes monthly throughout the year and Corporate Income tax monthly over a six month period beginning in February. Payments are based on Canada's Department of Finance's estimates for the taxation year, which are periodically adjusted until the income tax assessments or reassessments for that year are final. Income tax estimates, determined by the Government of Canada, combine actual assessments with an estimate that assumes that previous years' income tax allocations will be sustained and are subject to revisions in future years. Differences between current estimates and future actual amounts can be significant. Any such differences are recognized when the actual tax assessments are finalized.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(p) Taxes, regulatory, resource, and general revenues (continued)

Regulatory revenues, which are part of general revenues, are recognized on an accrual basis and include revenues for fines, fees, licenses, permits, and registrations. Amounts received prior to the end of the year, which relate to revenues that will be earned in a subsequent year, are recorded as deferred revenues and are recognized as revenue when earned.

Non-renewable resource revenue is recognized on an accrual basis and include mineral, quarry, oil and gas, and water license revenues as defined in the Northwest Territories Lands and Resources Devolution Agreement. Mineral and quarry revenues are collected under the authority of the NWT Lands Act, water revenues are collected under the authority of the Water Act and oil and gas revenues are collected under the authority of the Petroleum Resources Act. The Government is entitled to 50 percent of the Non-renewable resource revenues collected (which is referred to as the net fiscal benefit), up to a maximum amount based on a percentage of the Gross Expenditure Base under Territorial Formula Financing. The Government of Canada will deduct its share of the Non-renewable resource revenues collected by the Government (the remaining amount) from the Grant from the Government of Canada (note 2(n)) payable to the Government two years hence. The Government has also committed to sharing up to 25 percent of the net fiscal benefit with Aboriginal governments that are signatories to the Northwest Territories Lands and Resources Devolution Agreement as per the Northwest Territories Intergovernmental Resource Revenue Sharing Act.

Fuel, carbon, tobacco, payroll and property taxes are levied under the authority of the Petroleum Products and Carbon Tax Act, the Tobacco Tax Act, the Payroll Tax Act, and the Property Assessment and Taxation Act, respectively. Fuel, carbon and tobacco tax revenues are recognized on an accrual basis, based on statements received from collectors. Payroll tax is recognized on an accrual basis, based on payroll tax revenues of the prior year. Property tax and school levies are recognized on an accrual basis based on assessments of the prior year. Adjustments arising from reassessments are recorded in revenue in the year they are finalized.

Revenues from the sale of power and fuel riders are recognized in the period earned based on cyclical meter readings. All other revenues are recognized on an accrual basis.

Certain tangible capital asset additions of NT Hydro are made with the assistance of cash contributions from customers. These contributions are recorded as revenues when all external restrictions or stipulations imposed by an agreement with the external party related to the contribution have been satisfied, generally when the resources are used for the purposes intended.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(q) Expenses

Grants and contributions are recognized as long as the grant or contribution is authorized and eligibility criteria have been met. Grants and contributions include transfer payments paid through programs to individuals, and to provide major transfer funding for communities under community government funding arrangements. Payments to individuals include payments for children's benefits, income support or income supplement. Assistance is based on age, family status, income, and employment criteria. Other transfer payments are provided to conduct research, to establish new jobs through support for training and to promote educational, health and cultural activities. Also included are expenses of other consolidated entities and other miscellaneous payments. Under the authority of the Northwest Territories Intergovernmental Resource Revenue Sharing Act, a transfer to the Aboriginal parties who are signatories to the Northwest Territories Intergovernmental Resource Revenue Sharing Agreement will be made of up to 25 percent of the net fiscal benefit from Non-renewable resource revenues that is received by the Government (note 2 (p)). All other expenses are recognized on an accrual basis.

(r) Environmental liabilities

Environmental liabilities are contaminated sites, as a result of contamination being introduced into air, soil, water or sediment of a chemical, organic or radioactive material or live organism that exceeds an environmental standard. A liability for remediation of contaminated sites is recognized when all of the following criteria are satisfied: an environmental standard exists, contamination exceeds the environmental standard, the Government is directly responsible or accepts responsibility, it is expected that future economic benefits will be given up and a reasonable estimate of the amount can be made. The liability reflects the Government’s best estimate of the amount required to remediate the sites to the current minimum standard for its use prior to contamination.

Environmental liabilities consist of the estimated costs related to the management and remediation of environmentally contaminated sites, including costs such as those for future site assessments, development of remedial action plans, resources to perform remediation activities, land farms and monitoring. All costs associated with the remediation, monitoring and post-closing of the site are estimated and accrued. Where estimates are not readily available from third party analyses, an estimation methodology is used to record a liability when sufficient information is available. The methodology used is based on costs or estimates for sites of similar size and contamination when the Government is obligated, or is likely obligated, to incur such costs. If the likelihood of a future event that would confirm the Government's responsibility to incur these costs is either not determinable, or in the event it is not possible to determine if future economic benefits will be given up, or if an amount cannot be reasonably estimated, the contingency is disclosed in the notes to the consolidated financial statements and no liability is accrued. The environmental liabilities for contaminated sites are reassessed on an annual basis.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(s) Asset retirement obligations

On an annual basis, NT Hydro identifies legal obligations associated with the retirement of its tangible capital assets. Management's best estimate of the future expenditures required to settle the legal obligations are recognized to the extent that they can be reasonably estimated and are calculated based on the estimated future cash flows necessary to discharge the legal obligations, discounted using the NT Hydro's cost of borrowing for maturity dates that coincide with the expected cash flows.

The estimated asset retirement obligation (ARO) is recorded as a liability with a corresponding increase to tangible capital assets. The liability for AROs is increased annually for the passage of time by calculating accretion on the liability based on the discount rates implicit in the initial measurement. Changes in the obligation resulting from revisions to the timing or amount of the estimated undiscounted cash flows or revisions to the discount rate are recognized as an increase or decrease in the related carrying amount of the related tangible capital asset.

NT Hydro has identified AROs for certain hydro, thermal, transmission and distribution assets where NT Hydro expects to maintain and operate these assets indefinitely and therefore no related ARO has been recognized.

(t) Recoveries of prior years' expenses

Recoveries of prior years' expenses and reversal of prior years' expense accruals in excess of actual expenditures are reported separately from other revenues on the consolidated statement of operations and accumulated surplus. Pursuant to the Financial Administration Act, these recoveries cannot be used to increase the amount appropriated for current year expenses.

(u) Restricted assets

Restricted assets result from external restrictions imposed by an agreement with an external party, or through legislation of another government, that specify the purpose or purposes for which resources are to be used. Externally restricted inflows are recognized as revenue in the Government's consolidated financial statements in the period in which the resources are used for the purpose or purposes specified. An externally restricted inflow received before this criterion has been met is reported as a liability until the resources are used for the purpose or purposes specified.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(v) Segmented information

The Government reports on segments on the basis of relationships of its operations with similar entities. Segmented information is disclosed in Schedule B. Segments are identified by the nature of an entity's operations and the accountability relationship that a group of similar entities has with the Government. There are no significant allocations of revenues or expenses between segments.

Government departments are identified as one segment to reflect the direct accountability relationship for financial reporting and budgeting between departments, their respective Ministers and the Legislative Assembly.

Other Public Agencies within the Government Reporting Entity represent another segment. These agencies are typically associated with a particular Government department and have a formalized reporting relationship to that department. For example, Health and Social Services Authorities have an accountability relationship to the Minister of Health and Social Services as well as to their respective board members. Other Public Agencies also includes agencies that report directly to a Minister responsible for their operations. For example, the Northwest Territories Housing and Hydro Corporations have Ministers specifically assigned to their operations. The agencies in this segment assist the Government in delivering its programs and services and in achieving its priorities.

(w) Public Private Partnerships

The Government may, as an alternative to traditional forms of procurement governed by the Government’s Contract Regulations, enter into public private partnership (P3) agreements with the private sector to procure services and public infrastructure when: the total projected threshold for procuring those services, including capital, operating and service costs over the life of the agreement, exceeds $50,000; there is appropriate risk sharing between the Government and the private sector partners; the agreement extends beyond the initial capital construction of the project, and; the arrangement results in a clear net benefit to the Government as opposed to being merely neutral in comparison with standard procurement processes. The operating and service costs, that are clearly identified in the agreements, are expensed as they are incurred.

The Government accounts for P3 projects in accordance with the substance of the underlying agreements. In circumstances where the Government is determined to bear the risks and rewards of an asset under construction, the asset and the corresponding liability are recognized over time as the construction progresses. The capital asset (classified as work in progress) and the corresponding liability are recorded based on the estimated percentage of completion. In circumstances where the Government does not bear the risks and rewards of the asset until substantial completion the future associated agreement is disclosed.

The capital asset value is the total of progress payments made during construction and net present value of the future payments, discounted using the imputed interest rate for the agreement. Capital expenditures may occur throughout the project or at the capital in-service date. Service fees may occur throughout the project or when the project is operational; these fees will include both a service and operational component. All payments are adjusted to reflect performance standards as outlined in the specific agreement and penalties may be deducted for sub-standard performance. When available for use, the P3 assets are amortized over their estimated useful lives.

A P3 agreement may encompass certain revenues, including those collected by the partner on behalf of the Government. In such instances the Government will report the gross revenue along with the asset, liability, and expenses as determined from the specific project.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(x) Future accounting changes

Financial instruments

The Public Sector Accounting Board (PSAB) issued PS 3450 Financial Instruments effective for fiscal years beginning on or after April 1, 2022. Items within the scope of the standard are assigned to one of two measurement categories: fair value, or cost or amortized cost. Fair value measurement will apply to derivatives and portfolio investments in equity instruments that are quoted in an active market. Also, when groups of financial assets and financial liabilities are managed on a fair value basis they may be reported on that basis. Other financial assets and financial liabilities will generally be measured at cost or amortized cost. Until an item is derecognized, gains and losses arising due to fair value remeasurement will be reported in the Statement of Remeasurement of Gains and Losses. There will be no significant impact on the consolidated financial statements as a result of its application.

Other New Standards

Effective April 1, 2022, the Government will concurrently be required to adopt: PS 2601 Foreign Currency Translation, PS 1201 Financial Statement Presentation, and PS 3041 Portfolio Investments in the same fiscal period. Government organizations that apply PSAS were required to adopt these standards effective April 1, 2012, however there will be no significant impact on the consolidated financial statements as a result of its application.

Effective April 1, 2022, the Government will be required to adopt PS 3280 Asset Retirement Obligations. This standard provides guidance on how to account for and report liabilities for retirement of tangible capital assets. The Government is assessing the impact of this standard on the consolidated financial statements and anticipates that it will significantly impact Liabilities, Tangible Capital Assets, Opening Accumulated Surplus and Accumulated Amortization.

Effective April 1, 2023, the Government will be required to adopt PS 3400 Revenue. This standard provides guidance on how to account for and report on revenue. Specifically, it differentiates between revenue arising from transactions that include performance obligations and transactions that do not have performance obligations. There will be no significant impact on the consolidated financial statements as a result of its application.

Effective April 1, 2023, the Government will be required to adopt PS 3160 Public Private Partnerships. This standard provides guidance on how to account for and disclose public private partnerships. There will be no significant impact on the consolidated financial statements as a result of its application.

3. PORTFOLIO INVESTMENTS

4. DESIGNATED AND RESTRICTED ASSETS

Designated assets

Designated assets are included in cash and portfolio investments.

Pursuant to the Student Financial Assistance Act, the assets of the Student Loan Fund are to be used to provide financial assistance to post-secondary students that meet eligibility criteria as prescribed in its regulations.

Pursuant to the Northwest Territories Heritage Fund Act, the assets of the Heritage Fund are to be used to ensure that the future generations of people of the Northwest Territories benefit from on-going economic development, including the development of non-renewable resources.

Pursuant to the Waste Reduction and Recovery Act, the assets of the Environment Fund are to be used for purposes specified in the act including programs with respect to the reduction and recovery of waste.

Portfolio investments, while forming part of the Consolidated Revenue Fund, are designated for the purpose of meeting the obligations of the Legislative Assembly Supplemental Retiring Allowance Pension Plan (note 14). Supplementary Retiring Allowance Regulations restrict the investments to those permitted under the Pension Benefits Standards Act. The remainder consists of investments held by public agencies listed in note 1(a).

Pursuant to the Northwest Territories Business Development and Investment Corporation Act, and its Regulations, the Northwest Territories Business Development and Investment Corporation (BDIC) is required to establish a Loan and Investments Fund for its lending and investing activities. The regulations specify that a Loans and Bonds Fund will be used to record the lending operations. BDIC is required to use a Venture Investment Fund to record the venture investment operations. Furthermore, BDIC is obligated to maintain a Capital Fund and Subsidy Fund.

In addition to these funds, the BDIC is required, to establish a Capital Reserve Fund and a Venture Reserve Fund, respectively. The BDIC will continue to deposit to these reserve funds an amount equal to 10% of each capital or venture investment made. The BDIC may use these reserve funds for further investment or financing for its subsidiaries and venture investments through approved drawdowns.

Pursuant to the Land Titles Act, the assets of the Land Titles Assurance Fund are to be used to compensate owners for certain financial losses they incur due to real estate fraud or omissions and errors of the land registration system.

Other designated assets will be used for various specified purposes.

Restricted assets

Restricted assets include funds remitted to the Government, that are restricted for use in the Yellowknife Airport Capital Program, pursuant to the Memorandum of Agreement between the Government and Signatory Air Carriers. Restricted assets for Yellowknife Airport Improvement Fees at March 31, 2021 is

$7,793 (2020 - $7,420) and is included in cash and deferred revenue.

Notes to Consolidated Financial Statements

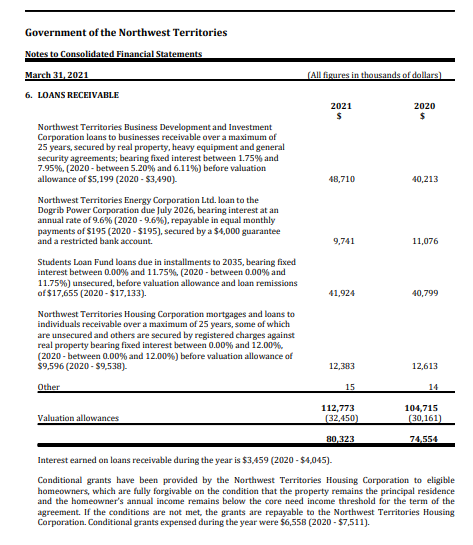

Interest earned on loans receivable during the year is $3,459 (2020 - $4,045).

Conditional grants have been provided by the Northwest Territories Housing Corporation to eligible homeowners, which are fully forgivable on the condition that the property remains the principal residence and the homeowner's annual income remains below the core need income threshold for the term of the agreement. If the conditions are not met, the grants are repayable to the Northwest Territories Housing Corporation. Conditional grants expensed during the year were $6,558 (2020 - $7,511).

7. SINKING FUND

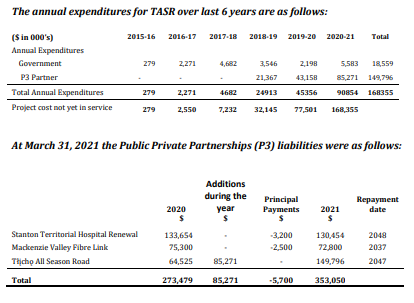

The Sinking Fund was established on July 15, 2019 and includes cash held in a separate bank account for the purpose of retiring liabilities under public private partnerships (note 13) for the Tlicho All Season Road contract. As at March 31, 2021, the Sinking Fund balance is $78,099 (2020 - $29,680); the carrying value approximates the market value. The weighted average effective rate of return for the year is 0.85% (2020 - 2.35%). Interest earned on the sinking fund during the year is $434 (2020 - $381).

As part of the Tlicho All Season Road contract, the Government will make a contribution of $33,910 to the Sinking Fund in 2022. In 2022, at the time of expected substantial completion, the Government will use the Sinking Fund to make a lump sum payment to retire a portion of the related liability under public private partnerships as described in note 13.

8. SHORT TERM LOANS

Based upon operational needs, the Government may enter into short term borrowing arrangements with its banks. Short term loans of $324,873 (2020 - $470,238) incurred interest at a weighted average year-end rate of 0.50% (2020 - 1.69%). Interest expense on short term loans included in operations and maintenance expenses is $2,389 (2020 - $8,294).

10. ENVIRONMENTAL LIABILITIES AND ASSET RETIREMENT OBLIGATIONS

The Government recognizes that there are costs related to the remediation of environmentally contaminated sites for which the Government is responsible. The Government has identified 277 (2020 - 278) sites as potentially requiring environmental remediation at March 31, 2021.

There were 7 (2020 - 11) sites closed during the fiscal year as they were either remediated or no longer meet all the criteria required to record a liability for contaminated sites.

Included in the 277 (2020 - 278) sites, there are 67 (2020 - 68) sites where no liability has been recognized. The contamination is not likely to affect public health and safety, cause damage, or otherwise impair the quality of the surrounding environment and there is likely no need for action unless new information becomes available indicating greater concerns, in which case, the site will be re-examined. These sites will continue to be monitored as part of the Government’s ongoing environmental protection program.

The asset retirement obligation includes NT Hydro's disposal of generating plants on leased land, storage tanks systems and the associated piping for petroleum products in all communities serviced by the Northwest Territories Power Corporation, a subsidiary of NT Hydro. The carrying amount of the obligation is based on total expected cash flows, expected timing of cash flows (majority to occur post 2089), and the weighted average discount rate of 2.40% (2020 - 2.48%) for obligations to be settled in 10 years or less and 3.12% (2020 - 3.11%) for obligations to be settled in 10 years or more.

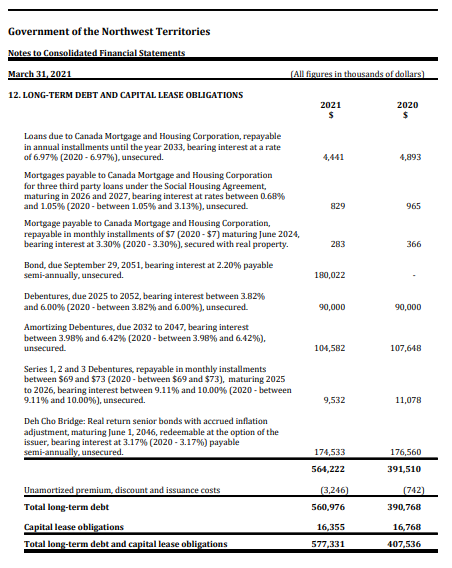

Interest expense on long-term debt, included in operations and maintenance expenses, is $20,037 (2020 - $20,611).

Interest expenses related to capital lease obligations for the year is $1,538 (2020 - $1,652), at an implicit average interest rate of 9.60% (2020 - 9.60%). Capital lease obligations (expiring between 2022 and 2061) are based upon contractual minimum lease obligations for the leases in effect as of March 31, 2021.

Debt Authority

The Government has the authority to borrow, pursuant to subsection 28(4) of the Northwest Territories Act (Canada), within a borrowing limit authorized by the Government of Canada. The Government borrowing limit was increased to $1,800,000 by Order in Council P.C 2020-0661, dated September 20, 2020.

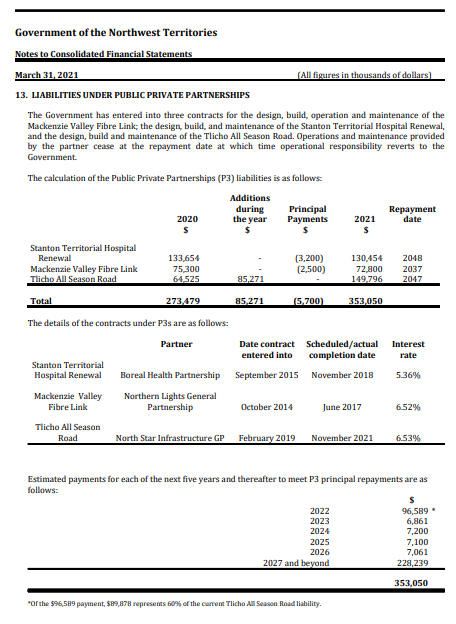

13. LIABILITIES UNDER PUBLIC PRIVATE PARTNERSHIPS (continued)

The capital payments for Mackenzie Valley Fibre Link and Stanton Territorial Hospital Renewal are fixed, equal monthly payments for the privately financed portion of the costs of building the infrastructure. The scheduled principal payments for Tlicho All Season Road will include the lump sum payment of $111.2 million in 2022 at the expected time of substantial completion and then fixed equal monthly payments thereafter. P3 interest expense for the year is $12,100 (2020 - $12,400). Interest capitalized in the period as a function of construction or developing tangible capital assets relating to the Tlicho All Season Road is $3,500 (2020 - $1,400).

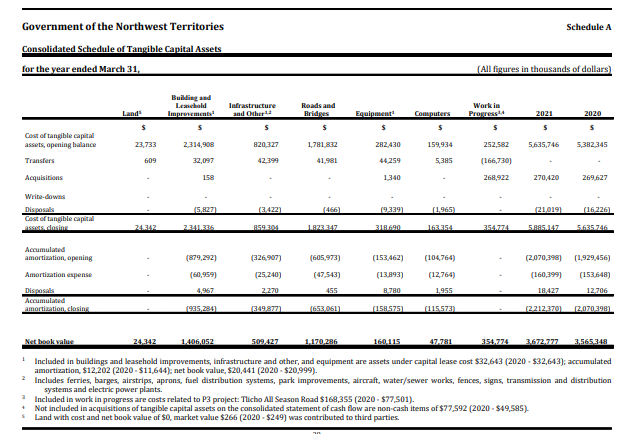

Tangible capital assets, commitments, and contractual rights related to P3 projects are disclosed in note 17 and schedule A.

14. PENSIONS

a) Plans' description

The Government administers Regular Pension Plans for Members of the Legislative Assembly (MLAs), Territorial Court Judges, Employees of the Hay River Health and Social Services Authority and the Employees, Superintendent and Assistant Superintendents of the Yellowknife Catholic Schools. These Regular Pension Plans are contributory defined benefit registered pension plans and are pre-funded (Regular Funded). The funds related to these plans are administered by independent trust companies.

In addition to the Regular Pension Plans listed above, the Government administers Supplemental Pension Plans for the MLAs, Territorial Court Judges and Superintendent and Assistant Superintendents of the Yellowknife Catholic Schools that are non-contributory defined benefit pension plans and are non-funded (Supplemental Unfunded). The Government has designated assets for the purposes of meeting the obligations of the MLA Supplemental Pension Plan (note 4). The supplemental Pension Plan for the Yellowknife Catholic Schools Superintendents and Assistant Superintendents is not funded until the employee terminates their employment from Yellowknife Catholic Schools.

The Government is liable for all benefits. All Plans provide death benefits to spouses and eligible dependents. All Plans are indexed. Plan assets consist of Canadian and foreign equities, and Canadian fixed income securities, bonds and mortgages.

Benefits provided under all Plans are based on years of service and pensionable earnings. Plan benefits generally accrue as a percentage of a number of years of best average pensionable earnings.

The remaining government employees participate in Canada’s Public Service Pension Plan (PSPP). The PSPP provides benefits based on the number of years of pensionable service to a maximum of 35 years. Benefits are determined by a formula set out in the legislation; they are not based on the financial status of the pension plan. The basic benefit formula is 2 percent per year of pensionable service multiplied by the average of the best five consecutive years of earnings.

The public service pension plan was amended during 2013 which raised the normal retirement age and other age related thresholds from age 60 to age 65 for new members joining the plan on or after January 1, 2013. For members with start dates before January 1, 2013, the normal retirement age remains age 60. Furthermore, contributions rates for current service for all members of the public service increased to an employer: employee cost sharing of 50:50 in 2017.

Other benefits include survivor pensions, minimum benefits in the event of death, unreduced early retirement pensions, and disability pensions.

14. PENSIONS (continued)

d) Pension expense

The components of pension expense include current period benefit cost, amortization of actuarial net (gains)/losses and interest on average accrued benefit obligation net of the expected return on average plan assets, change in valuation allowance and contributions from plan members. The total expense is $4,890 (2020 - $4,435). The interest cost on the accrued benefit obligation is determined by applying the discount rate determined at the beginning of the period to the average value of the accrued benefit obligation for the period. The expected return on plan assets is determined by applying the assumed rate of return on plan assets to the average market-related value of assets for the period. The difference between the expected and actual return on plan assets is a gain of $3,946 (2020 - $832).

In addition to the above, the Government contributed $58,053 (2020 - $55,229) to the Public Service Pension Plan. The employees' contributions to this plan were $56,454 (2020 - $53,356).

e) Changes to pension plans in the year

There have been no plan amendments, plan settlements and curtailments or temporary deviations from the plan in 2021.

f) Valuation methods and assumptions used in valuing pension liability

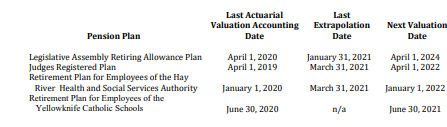

The following reflects the date of valuation for each plan for accounting purposes:

Liability valuation method

The actuarial valuations were performed using the projected accrued benefit method. The valuations are based on a number of actuarial assumptions about matters such as mortality, service, withdrawal, earnings and interest rates. The assumptions are based on the Government's best estimates of expected long-term rates and short-term forecasts.

14. PENSIONS (continued)

f) Valuation methods and assumptions used in valuing pension liability (continued)

Asset valuation method

The asset valuation method for all the plans is generally market-related value. The market value of the pension assets is $131,869 (2020 - $118,084).

Actuarial gains and losses

Actuarial gains and losses occur when actual experience varies from estimates or when actuarial assumptions change. The adjustments needed are amortized on a straight-line basis over the estimated average remaining service lives of the contributors.

15. OTHER EMPLOYEE FUTURE BENEFITS AND COMPENSATED ABSENCES

In addition to pension benefits, the Government provides severance (resignation and retirement), removal and compensated absence (sick, special, maternity and parental leave) benefits to its employees. The benefit plans are not pre-funded and thus have no assets, resulting in a plan deficit equal to the accrued benefit obligation.

Severance benefits are paid to the Government's employees based on the type of termination (e.g. resignation versus retirement) and appropriate combinations that include inputs such as when the employee was hired, the rate of pay, the number of years of continuous employment and age and the benefit is subject to maximum benefit limits. Removal benefits are subject to several criteria, the main ones being location of hire, employee category and length of service. The benefits under these two categories were valued using the projected unit credit methodology.

Compensated absence benefits generally accrue as employees render service and are paid upon the occurrence of an event resulting in eligibility for benefits under the terms of the plan. Events include, but are not limited to employee or dependent illness and death of an immediate family member. Benefits that accrue under compensated absence benefits, excluding maternity and parental leave, were actuarially valued using the expected utilization methodology. Non-accruing benefits include maternity and parental leave and are recognized when leave commences.

Valuation results

The most recent actuarial valuation was completed as at February 15, 2019 and the results were extrapolated to March 31, 2021. The effective date of the next actuarial valuation is March 31, 2022. The values presented below are for all of the benefits under the Compensated Absences and Termination Benefits for the consolidated Government.

16. TRUST ASSETS UNDER ADMINISTRATION

The Government administers trust assets on behalf of third parties, which are not included in the reported Government assets and liabilities. These consist of cash and term deposits of $20,068 (2020 - $17,815) which include Public Trustees and Securities for land use permits and water licenses and oil and gas.

In addition to the trust assets under administration, the Government holds cash and bank guarantees in the form of letters of credit and surety bonds in the amount of $666,425 (2020 - $678,637). The majority of these guarantees are held against water licenses issued to regulate the use of water and the deposit of waste.

18. GUARANTEES AND CONTINGENCIES

(a) Guarantees

The Government has guaranteed residential housing loans to banks totalling $322 (2020 - $380) and indemnified Canada Mortgage and Housing Corporation for third party loans totalling $6,426 (2020 - $8,203). In addition, the Government has provided a guarantee to the Canadian Blood Agency and Canadian Blood Services to cover a share of potential claims made by users of the national blood supply. The Government's percentage is limited to the ratio of the Northwest Territories' population to the Canadian population.

The Northwest Territories Business Development and Investment Corporation (BDIC) has one (2020 - one) outstanding loan to a Northern Community Futures organization totalling $318 (2020 - $339). Loans provided may be assigned to the BDIC when impaired. If assigned, the BDIC would then write-off the Northern Community Futures organization loan balance and would attempt to recuperate its loss. In 2021, no accounts were assigned to BDIC (2020 - $10).

The BDIC has one (2020 - two) outstanding irrevocable standby letters of credit totalling $2,000 (2020 - $2,100) that will expire in fiscal 2022. Payment by the BDIC is due from these letters in the event that the applicants are in default of the underlying debt. To the extent that the BDIC has to pay out to third parties as a result of these agreements, these payments will be owed to the BDIC by the applicants. Each letter of credit is secured by promissory note, general security agreement, guarantee or collateral mortgage. During the year, no payments were made (2020 - nil).

(b) Claims and litigation

There are a number of claims and pending and threatened litigation cases outstanding against the Government. In certain of these cases, pursuant to agreements negotiated prior to the division of the territories, the Governments of the Northwest Territories and Nunavut will jointly defend the suits. The cost of defending these actions and any damages that may eventually be awarded will be shared by the two Governments 55.66% and 44.34%, respectively.

The Government has recorded a provision for any claim or litigation where it is likely that there will be a future payment and a reasonable estimate of the loss can be made. The provision is based upon estimates determined by the Government's legal experts experience or case law in similar circumstances. At year-end, the Government estimated the total claimed amount for which the outcome is not determinable at $125,421 (2020 - $106,630). No provision for such claims has been made in these consolidated financial statements as it is not determinable that any future event will confirm that a liability has been incurred as at March 31.

21. OVEREXPENDITURE

During the year no departments (2020 - 1) exceeded their operations vote (2020 - $23) and no departments (2020 - 0) exceeded their capital vote (2020 - $0).

Over expenditure of a vote contravenes subsection 71 of the Financial Administration Act which states that "No person shall incur an expenditure that causes the amount of the appropriation set out in the Estimates for a department to be exceeded".

22. COVID-19

On March 22, 2020, the Government declared a public health emergency in response to the COVID-19 global pandemic. The Government implemented various programs and publicly announced supports and financial relief to individuals, businesses and organizations in response to the COVID-19 pandemic. The impact of COVID-19 on the Government's operations for 2021 is as follows:

Schedule A - Consolidated Schedule of Tangible Capital Assets

Schedule B - Consolidated Schedule of Segmented Information

Financial Statement Discussion and Analysis

INTRODUCTION

The Public Accounts report the financial position and results of operations of the Government of the Northwest Territories (Government) for a fiscal year. The information provided in the following pages is intended to assist readers of the Public Accounts in their assessment of the Government’s financial health.

The Consolidated Statement of Financial Position discloses the financial position of the Government including assets, liabilities, accumulated surplus or deficit, and the net debt position of the Government and is measured at March 31st.

The Consolidated Statement of Operations discloses financial information relating to revenues and expenses encompassing the results for a fiscal year.

The Consolidated Statement of Change in Net Debt explains the change in net debt. It tracks the extent to which expenditures of the accounting period are met by the revenues recognized in operations for the period; and what the Government has spent to acquire tangible capital assets and inventories.

The Consolidated Statement of Cash Flow discloses cash balances at the beginning and end of the fiscal year as well as the sources and uses of cash in operating, investing, financing and capital transactions during the fiscal year.

The information contained within the Consolidated Financial Statements (Public Accounts – Section I) includes all Government Departments and Government- controlled organizations (listed in Appendix A and Note 1 of the Consolidated Financial Statements) which collectively are referred to as the Government Reporting Entity (GRE).

EXECUTIVE SUMMARY

The consolidated results of operations for the fiscal year ended March 31, 2021 and the consolidated financial position as at March 31, 2021 is summarized below:

Note: Budget adjustments approved during the fiscal year are not reflected in the Public Accounts as the original approved budget is presented in accordance with Public Sector Accounting Standards (PSAS), see next page for discussion on approved budget adjustments.

-

The 2020-21 consolidated financial statements report an actual annual operating surplus of $90.2 million, which is $137.9 million or 60.5% lower than budgeted. The annual operating surplus is $167.6 million or 216.7% higher than the prior year. The change in the surplus is based on changes in revenue and expenses which is explained below.

-

Total consolidated revenue in 2020-21 is $2.4 billion, which is $43.2 million or 1.7% lower than the original budget. The total consolidated revenue is $314.6 million or 14.8% higher than the prior year. The increase in actual revenues is mainly due to an increase in the grant from Canada because of the Gross Expenditure Base increase as well as increased transfer payments from Canada related to COVID-19 funding.

-

Total consolidated expenses in 2020-21 are $2.4 billion, an increase of $94.8 million or 4.2% from the original budget. The total consolidated expenses are $147.0 million or 6.7% higher than the prior year. The increase in actual expenses is due primarily to the impact of COVID-19 expenditures related to financial support programs for economic relief and the implementation of health and safety measures.

-

The Government is in a net debt position of $1.3 billion. During the year, the Government issued $180.0 million in bonds, incurred $85.3 million in P3 obligations, and incurred $23.6 million in deferred revenues which increased net debt. The Government used $140.0 million of the bond proceed to retire short term loans and invested $48.4 million into a sinking fund which reduced net debt. Combined with other changes in financial assets and liabilities, net debt increased by $27.1 million during the 2020-21 fiscal year.

-

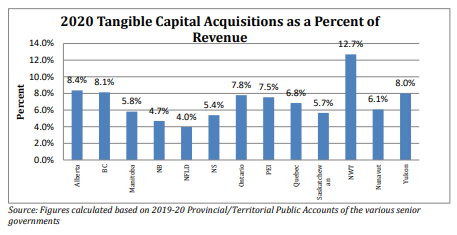

Non-Financial Assets increased by $117.3 million or 3.2% over prior year. A total of $270.4 million was incurred to acquire assets: $90.9 million was added to the work in progress on the Tlicho All Season Road; $7.2 million was added as refurbishment of Stanton Legacy Building; and the residual was for various roads and bridges, community health centres and equipment.

Budget adjustments, which are approved through supplementary appropriations, should be considered before any conclusions are drawn with respect to operational results as budget adjustments made during the fiscal year typically reflect new information that is not known at the time the original budget is approved.

Factoring in approved budget adjustments, the 2020-21 Consolidated Financial Statements report an actual annual operating surplus of $90.2 million, which is

$99.7 million more than the revised deficit budget of ($9.4) million as shown below:

-

Total consolidated revenue in 2020-21 is $2.4 billion, which is $35.2 million lower than the revised revenue budget of $2.5 billion. There were increases of $113.5 million in the revised revenue budget for cost shared transfer payment. These increases were partially offset by budget decreases of $44.8 million in taxation revenue, $26.2 million in general revenues and $89.2 million in Federal infrastructure transfers resulting from the Government foregoing revenues through abatements to ease the burden of the COVID-19 pandemic.

Total consolidated expenses in 2020-21 are $2.4 billion. This is $134.9 million lower than the revised expense budget of $2.5 billion. The revised budget was increased to address the impact of COVID-19 expenses related to financial support programs for economic relief and the implementation of health and safety measures including the newly formed COVID-19 Secretariat enforcement and compliance programs.

The past fiscal year was unprecedented globally due to the COVID-19 pandemic, which significantly impacted economies due to worldwide shutdowns. The Northwest Territories (NWT) was not immune to these impacts of the global COVID-19 pandemic as evidenced by the significant impacts on revenues as well as expenses.

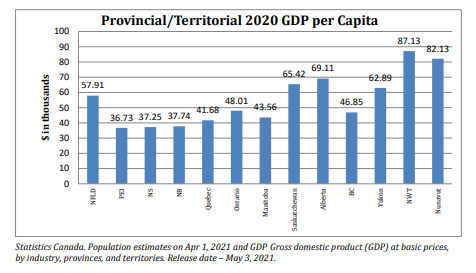

Even before the COVID-19 pandemic, the Northwest Territories economy experienced a contraction which had an impact on revenues in 2021. Per Statistic Canada, the real Gross Domestic Product of the territory is estimated to have declined 10.4% in 2020 (the latest figures available), compared to the national decline of 5.3%. The 2020 real GDP decline is attributed to lower production from the diamond mines, which in turn resulted in a decline in the transportation and warehousing sector.

FINANCIAL HIGHLIGHTS

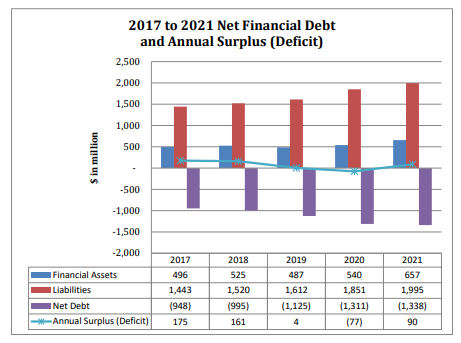

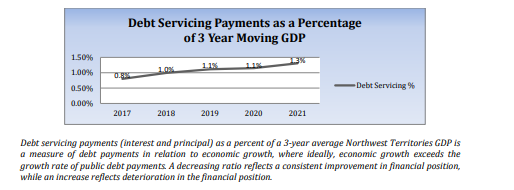

Accumulated Surplus /Deficit and Net Financial Debt

At the end of the 2021 fiscal year, the Government is in a net debt position as liabilities exceeded financial assets and net debt increased during the fiscal year. This increase is primarily attributable to increase in liabilities related to public private partnerships (P3). The change in net debt is shown on the Consolidated Statement of Change in Net Debt within Section 1 of the Public Accounts.

The graph below illustrates the Government’s net debt position and annual surplus/deficit at the end of each of the last five fiscal years:

Net assets result when there are financial assets remaining after deducting all liabilities of the Government. Net debt results when liabilities are more than financial assets. Net debt represents the debt burden on future generations that must be recovered through either future revenues or future service reductions.

Cash Flow and Cash Position

The Consolidated Statement of Cash Flow reports on the sources and uses of cash during the fiscal year. The Government’s cash position increased by $30.4 million; from $85.5 million in 2020 to $115.8 million in 2021. The cash position improved in fiscal 2021 due to $ 260.8 million cash flows from operations, and $17.0 million cash flows from financing transactions. This was off set by $ 55.2 million cash used in investing transactions and $192.2 million used in capital transactions.

Cash is used to meet operational expenses, reduce liabilities and to pay for the Government’s investment in infrastructure. More detail is available on the Statement of Cash Flows within Section I of the Public Accounts.

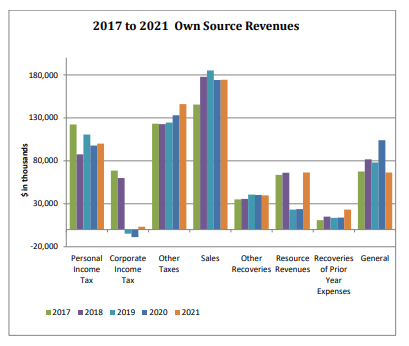

Financial Assets

Financial assets represent the amount of resources available to the Government that can be converted to cash to meet obligations or fund operations.

Approximately 17.6% of the Government’s financial assets are cash. The 82.4% balance of the financial assets, varying from relatively short-term investments and inventory for resale to long-term loans receivable, is convertible to cash and will, over time, contribute to the Government’s ability to discharge its liabilities.

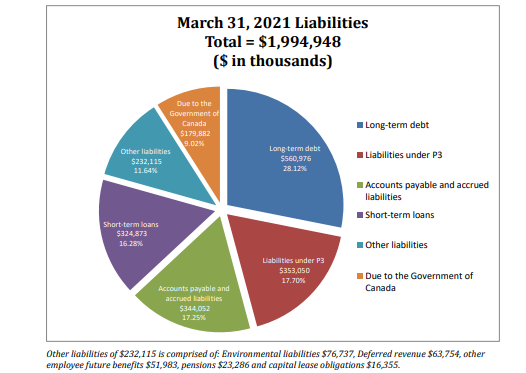

Liabilities

Liabilities represent the obligations the Government has to others. The graph below illustrates the composition of the Government’s liabilities:

he Government presently has $656.9 million in financial assets available to discharge liabilities of $2.0 billion. The gap between the Government’s financial assets and its liabilities, also referred to as net debt, indicates that some of its future revenues will be required to meet these obligations.

Short-Term Loans

The Government enters short-term borrowing arrangements. The short-term loans balance decreased by 31.0% from prior year as a result of short-term loans that were converted to long-term loans by issuing a debenture.

Accounts Payable and Accrued Liabilities

Accounts payable and accrued liabilities include obligations to pay for goods and services acquired prior to year end. Accounts payable and accrued liabilities increased by $10.9 million; from $333.2 million in 2020 to $344.1 million in 2021. The increase is mainly attributable to more expenses incurred in 2021 compared to 2020.

Pensions and Employee Future Benefits

The Government administers Regular and Supplemental Pension Plans for Members of the Legislative Assembly (MLAs), Territorial Court Judges and the Employees, Superintendent and Assistant Superintendents of the Yellowknife Catholic Schools. The Government also administers Regular Pension Plans Employees of the Hay River Health and Social Services Authority. These plans are comprised of contributory and non-contributory defined benefit pension plans and are administrated by independent trust companies.

All eligible remaining Government employees participate in Canada’s Public Service Pension plan, a contributory defined benefit pension plan that is administered by the Government of Canada.

At year end the pension liability was comparable with prior year and detailed information can be found within Section 1 of the Public Accounts (note 14).

Employee future benefits for sick, special, leaves as well as severance benefits for retirement, resignation, and removal, accrue for Government employees as service is rendered. Maternity and parental benefit leaves are non-accruing and paid when the leave commences. These benefits are paid to eligible employees on the occurrence of an event resulting in eligibility for benefits such as termination. An actuarial evaluation is completed periodically (generally every 3 years) to determine the value used for Employee future benefits in the Public Accounts for the GRE.

At year end the employee future benefits liability is $51.9 million a decrease of 12.2% from prior year. The decrease is due to lower termination benefits by $4.7 million, removal benefits by $0.9 million and compensated absences by $1.5 million resulting mainly from NTHSSA and Government departments: Health, Infrastructure and Justice. Benefit payments were higher than expected.

Environmental Liabilities

The nature of the Government’s programs and services exposes the Government to costs associated with remediation of any site contamination that occurred because of government operations. These costs make up the Environmental Liabilities amount disclosed within Section 1 of the Public Accounts (note 10). In addition, the liability may include contaminated sites where the Government does not own the site but has accepted responsibility. A summary of the Government’s policy with respect to Environmental Liabilities can be found within Section 1 of the Public Accounts (note 2r).